Before the first volatility ETF could be launched in 2009, some major achievements were necessary.

1973: Implied Volatility

Options on stocks had been around for some time, but there was no universally accepted method to value an option.

In 1973, Fischer Black and Myron Scholes published “The Pricing of Options and Corporate Liabilities”. Robert Merton published another significant paper on this subject.

The Black-Scholes-Merton model uses six parameters to price an option:

- Current price of the underlying

- Strike price of the option

- Time to expiration

- Dividend rate

- Risk-free rate

- Implied volatility

Except for implied volatility, all parameters can be observed in the market. Implied volatility is the expected volatility between now and expiration.

The Black-Scholes-Merton model ignited a boom in options trading. As a result, market participants became interested in measuring implied volatility.

Late 1980s – Early 1990s: VIX

VIX is short for the Chicago Board Options Exchange’s CBOE Volatility Index. This index measures the market participants’ expectation of volatility (= “implied volatility”) based on the prices of S&P 500 index options.

While stock market indices had been used for decades, a measure of expected volatility was not available. Menachem Brenner and Dan Galai published a break-through article in the Financial Analysts Journal in 1989. The authors referred to their volatility index as “Sigma Index”.

Building on the work of Brenner and Galai, Bob Whaley used CBOE index options data series to calculate the VIX.

2003: New VIX Methodology

The original VIX was based on CBOE S&P 100 index (OEX) options. CBOE, with the help of Goldman Sachs, came up with a new methodology, using CBOE S&P 500 index (SPX) options instead.

Overall, the VIX levels calculated by the two methodologies do not differ too much.

2004: VIX Futures

A significant step towards the availability of volatility ETPs was made in 2004. Until then, the VIX was just an index, but could not be traded.

On March 26, 2004, trading in VIX futures started. Two years later, VIX options were launched.

2009: VXX Inception

The first-ever VIX ETP was launched on January 30, 2009. In line with all other major volatility ETPs ever launched, VXX does not track the spot VIX, but the 30-day blend of first and second month VIX futures.

In the midst of the Global Financial Crisis, the market was ready for an ETP that provided exposure to a long VIX futures position. Unfortunately, VXX appeared towards the end of the bear market and lost almost 70% of its value through the end of 2009.

As options on ETF are popular, it does not come as a surprise that VXX options were launched in 2010.

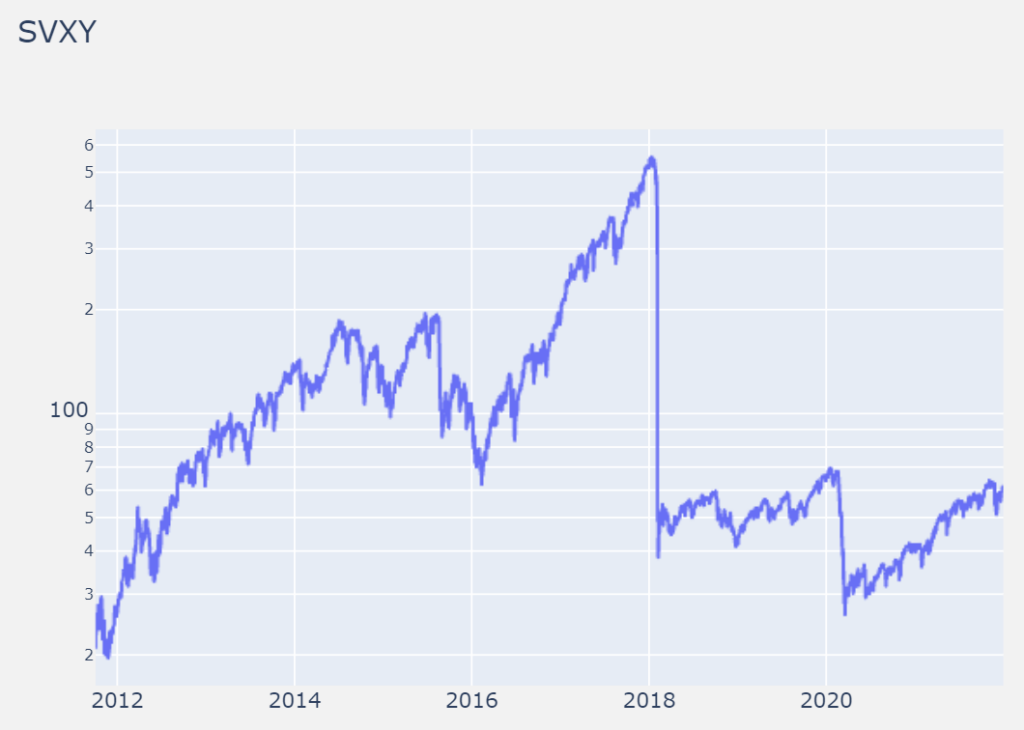

2018: Volmageddon

2017 was a year with historically low VIX levels. As a result, short-volatility ETFs such as XIV and SVXY went up 188%. Many investors were attracted by this meteoric rise, and many did not understand the risks associated with holding these short-volatility ETFs.

Suddenly, on February 5, 2018, volatility returned to the market with a vengeance. This apocalyptic event is known as “Volmageddon”.

The S&P 500 dropped 4% in a single day – and XIV/SVXY lost around 15% during regular trading hours. Disaster struck after regular trading hours, when – according to prospectus – these volatility ETFs started trading VIX futures for their daily rebalancing between 4pm and 4:15pm.

The next day, XIV and SVXY opened roughly 90% lower. XIV was delisted on February 15, as the so-called termination event (daily loss in excess of 80%) had been triggered.

SVXY continued trading, though with a lower leverage factor (0.5x vs 1x).

UVXY, the popular long-volatility ETF, was affected too: its leverage factor was decreased from 2x to 1.5x, effective February 28, 2018.

2020: Extreme Moves During COVID-19 Panic

Long-volatility ETFs demonstrated in February/March 2020 that (when timed correctly) they can deliver sizeable returns and portfolio protection.

For example, 2x leverage long-vol TVIX shot up from $40 to (intraday) $1,000.

Unfortunately, the highly popular TVIX has since been added to the ever-growing list of retired volatility ETFs.

2022: SVXY, VXX and UVXY

A lot has changed since the inception of VXX, the first volatility ETP. Currently, the most frequently traded volatility products are:

- SVXY (0.5x leverage short-volatility ETF)

- VXX (1x leverage long-volatility ETN)

- UVXY (1.5x leverage long-volatility ETF)

Interested in learning more about volatility products?

- “Exotic” and thinly traded volatility ETFs

- Difference between ETN and ETF volatility products